Like “assault rifles,” predatory lending is one of those concepts on which no one can agree. Generally, applying unfair, dishonest, or abusive loan terms to customers is known as predatory lending. Be aware, though, that the description is nearly as concise as explanations of the Holy Ghost’s precise nature. There is a lot of hesitation and often conflicting justifications. However, no one seems to concur on a single, clear-cut definition.

So why don’t we take that term for a spin and see predatory lending for what it really is – lending?

What is Predatory Lending for real?

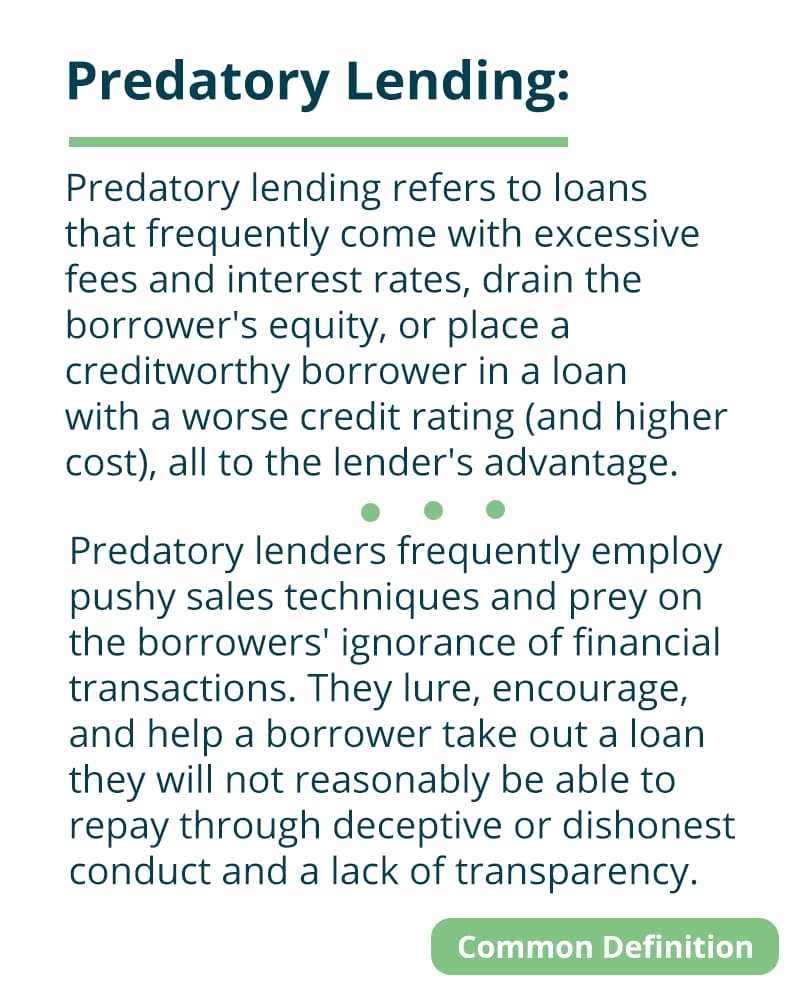

Before taking it apart, let us first examine the wide-known concept of the phenomenon, supported by some major authorities in the financial world.

This depiction is often the best you will come up with in the offline and online world. However, nothing really points specifics out that differ much from lending itself.

Does that make lending, in general, predatory?

If you are to follow the Wikipedia explanation, there is a list of signs and practices given as exemplary. You might also note the following two:

- Failure to present the loan price as negotiable.

Pause and ask yourself when was the last time you negotiated for a loan rate at a bank. It was likely never, similar to how you would not haggle over gas prices at a gas station. You can accept or reject the prices that are posted, and that is it. As it covers almost all loans, this term is either meaningless or proof in our direction that each loan is, by definition, predatory. Still, let us look into the second sign.

- Unjustified risk-based pricing.

Suppose you are applying for a car loan. Your credit score will inevitably and directly impact the interest rate you pay for that loan. What is more, that is a non-negotiable again—another point in the wrong basket.

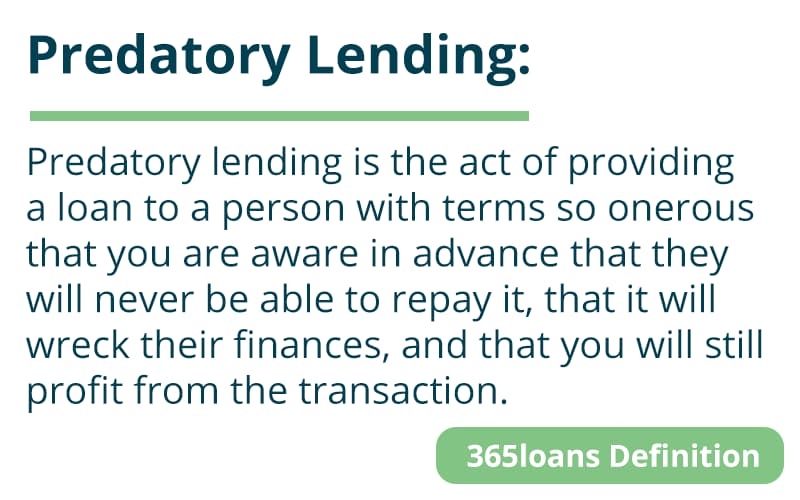

So, what is predatory lending for real?

How does Predatory Lending work?

Because most people choose to ignore anything that cannot be presented in a sound bite, issues like predatory lenders exist. Unfortunately, anyone can play the game of predatory lending, from the extremely wealthy to the really poor. And indeed, much to their dismay, the middle class frequently treads in this uncharted area.

Let us examine a few instances:

- Predatory Lending and Payday Loans.

Suppose you know a guy named Bill. Bill takes money on his next week’s paycheck since he cannot manage his finances or wait a few days for his pay. Due to having to repay the loan from the prior week, he runs out of money even sooner the following week. He proceeds to take out another loan, and the cycle continues. He quickly transitions to borrowing every payday for the next payday.

Bill is blind to the fact that when these loans are combined, their interest rates range from 100 to 300 percent. He will undoubtedly be laid to rest by them.

The lender is aware that Bill will not be able to repay his payday loan and will have to get another one, which will cause him to file for bankruptcy eventually. So, finally, he stops making payments on the loan. But, of course, the lender has already received far more in interest payments than the loan’s original principal. So in just a few months, he most likely received a 200% return on his investment. And in bankruptcy, he will gain more.

When Bill files for bankruptcy, the judge orders him to “work out” his debts over the course of the following five years. Bill pays off his “debt” to the payday loan company in periodic payments. Of course, another provider of payday loans will offer to lend him money, and why not? Bill has another seven years before he can file for bankruptcy. They’ve got him. And since his credit is terrible, he cannot borrow money from anywhere else. So much for Bill trying to bargain rates!

Payday loans are a prime illustration of predatory lending done right. Predatory lending is not just for the impoverished; the middle class can also participate.

- Predatory Lending and Car Loans.

Suppose your dear friends, Ted and Kathryn, decide to buy an RV. A lender offers a 10-year loan at what seems to be advantageous interest rates (7% or higher) to “get them into” the RV. Ted and Kathryn are, of course, “upside down” for most of the loan’s period because the RV loses value faster than the loan sum.

Really, Ted and Kathryn just wanted the RV for a short time. So, they want to sell after five years because they are sick of camping. They cannot, though. By virtue of the debt, they are bound. The loan balance has a deficit that is in the tens of thousands of dollars. They would need to come up with this sum first, which they lack because they are employees with average pay.

Even if they could file for bankruptcy, the lender would likely receive most, if not all, of their money back when the debt was “worked out” in bankruptcy court. As a result, the RV stays in the backyard while they endure another ten years of excruciating payments. The danger of default is low, and the lender receives a healthy return on its investment. They received no explanation from anyone at the lending firm on how this might occur to them.

And to your surprise, we reach the third example with wealthy people as the main characters, supposedly smart about their finances.

- Predatory Lending and Serial Refinancing.

Suppose you went to a legal conference where you met Jack and Jill, a charming family dressed in formal attire. The total salary of Jack and Jill, who both work as attorneys for a sizable company in Orlando, Florida, was in the hundreds of thousands of dollars. They have refinanced their mini-mansion in Thornton Park no less than five times, as Jill confides to you while laughing.

They are unable to save any money despite their incredible salary. They both went into buying leased automobiles, smartphones, and luxury clothing for themselves and their kids. Jack and Jill insisted on leading the lifestyle they believed they were entitled to. They racked up credit card debt as a result, and when it got to be too much to handle, they borrowed against the equity in their house to pay it off. So, they did and added thousands to the loan total each time they refinanced due to junk fees and closing expenses, which therefore affected their net worth.

Although they looked like having a luxurious lifestyle, they did not. And they could continue their juggling act as long as they could afford their enormous incomes. But for the sake of the story, one of them loses his job, at which point Jack and Jill refuse to take that the fancy life is over. Therefore, instead of acknowledging they are in debt, they withdraw money from their 401(k) to pay their mortgage, believing that “things will be better soon.” They use their life savings to pay interest to the bank, ending up utterly bankrupt in a few years.

How to avoid Predatory Lending?

All three exemplary situations, of course, have one thing to say in common: people voluntarily agree to take out these loans.

Bill wanted a six-pack of beer more than he “needed” a payday loan. Likewise, an RV was not a “need” to Ted and Kathryn. And Jack and Jill felt entitled to all the luxuries and gadgets in their life, even if they did not need them.

You can elect not to sign such loan agreements and leave your pen at home. You would be shocked. You think you need many things in life when they are really wants.

You can choose to stay within your means of earnings. However, perpetual debt is not a great option, as borrowing money will never benefit you financially. Therefore, you can assume that all lending could turn out to be predatory lending by nature.